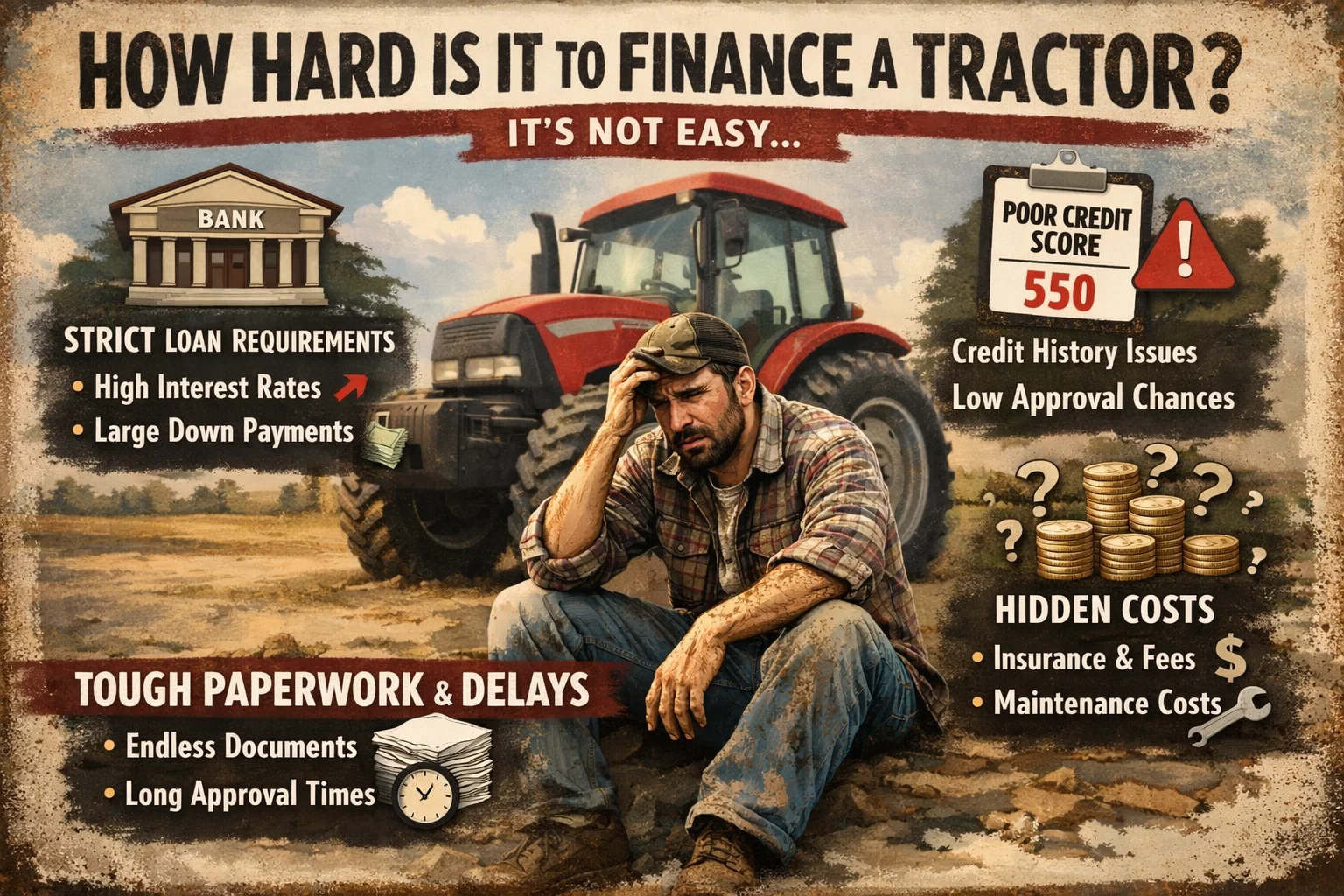

Buying a tractor is a major decision, whether you are a small-scale farmer, a landowner, or a contractor expanding operations. One of the first questions people ask is how hard is it to finance a tractor, especially with rising equipment prices and stricter lending rules. The answer is not one-size-fits-all. Tractor financing depends on several factors, including credit score, income stability, tractor type, lender policies, and down payment capacity.

This guide walks you through the realities of tractor financing in a clear, honest way. You will learn what lenders look for, what makes approval easier or harder, and how to improve your chances. By the end, you will know exactly what to expect and how to move forward with confidence.

Understanding Tractor Financing Basics

How hard is it to finance a tractor, Tractor financing works much like vehicle or equipment loans, but with agricultural-specific considerations. Lenders typically classify tractors as agricultural equipment, which can offer longer repayment terms than standard auto loans. Financing options include banks, credit unions, equipment manufacturers, and specialized agricultural lenders.

The difficulty level largely depends on your financial profile and the type of tractor you want. How hard is it to finance a tractor, New tractors are generally easier to finance because they hold predictable value, while used tractors may require higher interest rates or shorter loan terms. Lenders also consider whether the tractor will generate income or be used for personal land maintenance. Understanding these basics helps set realistic expectations before applying.

Is Financing a Tractor Hard Compared to Other Equipment?

When comparing tractors to other heavy equipment, financing is often moderately easier. Tractors have a strong resale market, making them less risky for lenders. This resale stability allows financing terms that can stretch from 36 to 84 months, depending on the lender.

How hard is it to finance a tractor, However, tractors are still more complex to finance than passenger vehicles. Loan amounts are higher, and lenders often request business documentation or farm income records. If you have a stable income and a clear use case, approval is usually straightforward. Difficulty increases when income is irregular, credit is weak, or the tractor is very old. Overall, tractor financing sits in the middle range of lending difficulty.

Credit Score Requirements for Tractor Loans

How hard is it to finance a tractor, Your credit score is one of the strongest factors influencing approval. Most lenders prefer a score of 650 or higher, though some manufacturer-backed programs approve borrowers with scores in the 600–640 range. A higher score unlocks lower interest rates, smaller down payments, and longer terms.

If your score falls below 600, financing is still possible but becomes more challenging. You may face higher interest rates, stricter repayment schedules, or the need for a co-signer. How hard is it to finance a tractor, Lenders also look beyond the number, reviewing payment history and debt levels. A solid credit profile significantly reduces how hard the financing process feels.

Income and Employment Stability

How hard is it to finance a tractor, Lenders want reassurance that you can repay the loan consistently. For farmers, this often means providing tax returns, profit-and-loss statements, or crop income records. For non-farming buyers, pay stubs or business income documentation may be required.

Stable, predictable income makes financing much easier. How hard is it to finance a tractor, Seasonal income is common in agriculture, and many lenders understand this, but they still want proof of long-term viability. New farmers or startup operations may face more scrutiny. Showing multiple income sources, such as off-farm employment, can strengthen your application and reduce perceived risk.

New Tractor vs Used Tractor Financing

How hard is it to finance a tractor, The choice between a new or used tractor has a major impact on loan difficulty. New tractors are easier to finance because their value is known and depreciation is predictable. Manufacturers often offer low-interest or promotional financing, especially during planting or harvesting seasons.

Used tractors, while cheaper upfront, can be harder to finance. How hard is it to finance a tractor, Lenders may limit loan terms or require larger down payments due to uncertainty about condition and lifespan. Very old tractors may not qualify at all. If financing ease is a priority, newer models typically provide smoother approval and better overall terms.

Down Payment Expectations

Down payments reduce lender risk and directly influence loan approval. Many tractor loans require 10% to 20% down, though some promotional programs allow zero-down financing for well-qualified buyers.

A larger down payment lowers monthly payments and interest costs, making financing easier to manage. How hard is it to finance a tractor, Buyers with weaker credit often need higher upfront contributions. While not always mandatory, a down payment signals commitment and financial responsibility. Preparing cash in advance can dramatically reduce how hard the financing process feels and improve approval odds.

Interest Rates and Loan Terms Explained

Interest rates for tractor financing vary widely based on credit score, loan length, and lender type. Manufacturer financing can offer rates as low as 0% to 4%, while banks and credit unions typically range from 5% to 9%. Higher-risk borrowers may see double-digit rates.

Loan terms usually fall between 3 and 7 years, with longer terms lowering monthly payments but increasing total interest. Choosing the right balance is crucial. Understanding these mechanics helps you evaluate offers clearly and prevents surprises later in the repayment period.

Lender Types and Their Approval Standards

How hard is it to finance a tractor, Different lenders approach tractor financing with different risk tolerances. Manufacturer lenders are often the easiest option, as they understand equipment value and usage. Banks and credit unions may offer competitive rates but require stronger documentation.

Agricultural finance companies specialize in farm equipment and are more flexible with seasonal income. Online lenders provide speed but often charge higher rates. Selecting the right lender for your profile reduces friction and simplifies approval. Knowing where to apply can make the difference between an easy experience and a frustrating one.

How Hard Is It to Finance a Tractor for First-Time Buyers?

How hard is it to finance a tractor, First-time tractor buyers often worry about approval, but financing is not impossible. The challenge comes from limited borrowing history with equipment loans. Lenders compensate by focusing more heavily on income stability and credit behavior.

Providing a clear explanation of tractor use, whether for farming, landscaping, or property maintenance, helps lenders assess risk. First-time buyers with decent credit and steady income are often approved without major issues. Preparation and documentation are key to making the process smoother and less intimidating.

Financing Challenges for Small Farms and Hobby Farmers

How hard is it to finance a tractor, Small farms and hobby farmers face unique hurdles. Income may be lower or inconsistent, making lenders cautious. However, many lenders recognize the growing trend of part-time agriculture and adapt their requirements accordingly.

Showing alternative income sources, strong savings, or land ownership improves approval chances. Financing may require slightly higher rates or shorter terms, but it is still achievable. Understanding lender expectations helps hobby farmers navigate the process confidently without feeling discouraged.

Steps to Improve Tractor Financing Approval Odds

Preparation is the most powerful tool. Start by reviewing your credit report and resolving any errors. Reduce outstanding debt where possible and gather income documentation early. Comparing lenders helps you identify the most flexible options.

Applying with a co-signer, increasing your down payment, or choosing a slightly lower-priced tractor can dramatically improve outcomes. These steps turn financing from a stressful challenge into a manageable process with predictable results.

Common Mistakes That Make Tractor Financing Harder

Many applicants unintentionally complicate financing. Applying without documentation, choosing an overvalued tractor, or ignoring credit issues can lead to rejection. Some buyers focus only on monthly payments, overlooking total loan cost.

Another common mistake is applying with multiple lenders simultaneously, which can impact credit scores. Being strategic and informed avoids these pitfalls. Awareness helps you approach financing calmly and increases the likelihood of favorable terms.

Conclusion

So, how hard is it to finance a tractor? For most buyers, it is moderately easy when preparation meets realistic expectations. Strong credit, stable income, and a clear use case significantly reduce difficulty. Challenges arise mainly from weak credit, insufficient documentation, or unrealistic equipment choices.

With the right lender and proper planning, tractor financing becomes a practical step rather than a barrier. Understanding the process empowers you to make informed decisions, secure fair terms, and invest confidently in equipment that supports your long-term goals.

Frequently Asked Questions

Is tractor financing easier than a car loan?

Tractor financing is slightly more complex due to higher loan amounts, but longer terms often balance the difficulty.

Can I finance a tractor with bad credit?

Yes, but expect higher interest rates or the need for a co-signer or larger down payment.

Do tractors qualify for zero-down financing?

Some manufacturer programs offer zero-down options for buyers with strong credit profiles.

How long does tractor loan approval take?

Approval can take anywhere from 24 hours to one week, depending on lender and documentation.

Is financing a used tractor worth it?

It can be, but terms are usually stricter and interest rates higher than for new tractors.

Does tractor financing require business registration?

Not always. Personal financing is available, but business use may require additional paperwork.

For More Update and Stories Visit Daily Guides